Due to market volatility, world events and Ofgem’s new methodology, our price cap prediction has changed.

Please see the latest predictions via our blogs page here

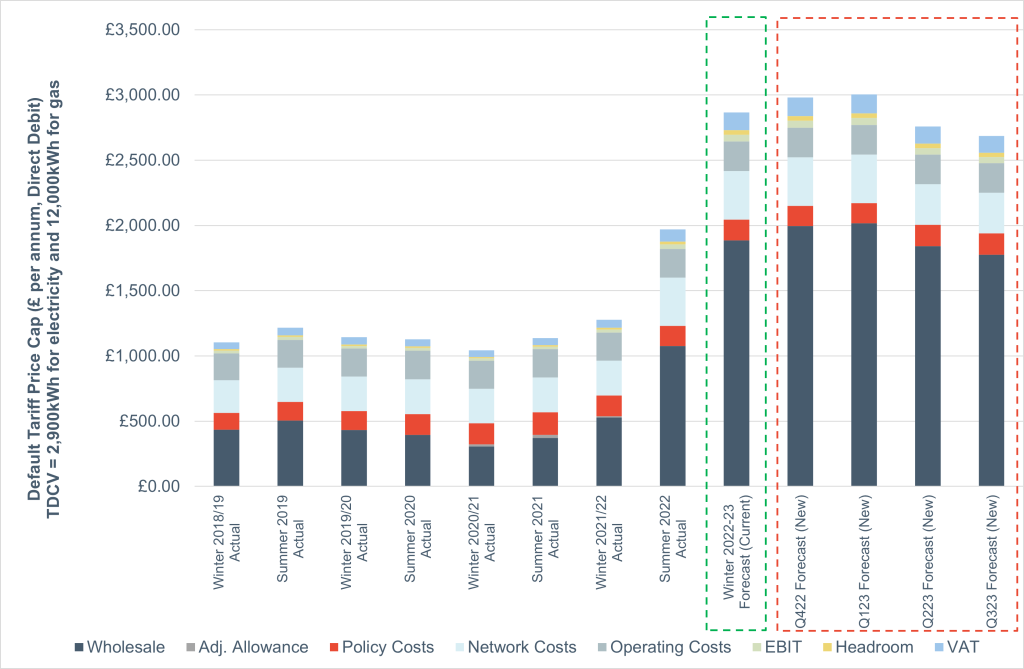

This week Cornwall Insight released its updated forecasts for the Default Tariff Cap. Q1 2023 which runs from January to March rose to over £3,000 for a typical user, the highest Cap we have ever seen, with the last quarter of 2022 Q4 running from October to December predicted to be £2,980. The rise means an average household will pay just under £3,000 across the component quarters of the coming winter.

The increase is primarily led by a rise in gas prices. These have climbed in response to the latest wholesale market uncertainty surrounding flows from Russia into Continental European markets with reductions in deliveries in Germany, Italy and Austria, among others being observed.

While Cornwall Insight are still forecasting a drop in the cap for Summer 2023, predictions have risen in absolute terms over the past few weeks across all periods, reflecting higher wholesale prices across the traded market.

These predictions do not include the impact of the Energy Bills Support Scheme announced by the government earlier this year.

Figure 1: Cornwall Insight’s default tariff cap forecasts

| QUARTERLY | Q4 2022 CI Forecast | Q1 2023 CI Forecast | Q2 2023 CI Forecast | Q3 2023 CI Forecast |

| Electricity | 1384.52 | 1399.75 | 1346.57 | 1315.53 |

| Gas | 1596.11 | 1603.45 | 1411.76 | 1370.19 |

| TOTAL | 2980.63 | 3003.20 | 2758.33 | 2685.71 |

| AVERAGE | 2991.92 | 2722.02 |

Figure 2: Default Tariff Price cap levels chart since 2018 and Cornwall Insight’s predictions for the next four cap rises

Source: Cornwall Insight

With the geopolitical events in Russia and subsequent barriers to energy flows having a significant impact on the wholesale market, and the situation showing no sign of abating, we are unfortunately predicting average consumers will be facing a bill over 50% more than the existing cap – itself an unprecedented rise.

While the UK gets very little energy from Russia, ultimately the countries that do are seeking alternative sources of gas. This will impact the energy flows to the UK from Continental Europe and cause further volatility in the market, adding fresh upward pressure to prices.

While the government has offered families some respite through their Energy Bills Support Scheme, this is not an enduring solution. Our predictions say high bills are to last for at least the coming 12 to 18 months – what will happen in January or April 2023 when the extra funding is not available? Longer-term solutions, including increasing energy security through investments in renewables, will lead to the UK becoming less reliant on energy imports – subsequently meaning the volatile wholesale market will have a lower impact on UK bills. Of course, this is of little comfort to those struggling right now.

In the shorter-term we need to see a review of funding to support those in fuel poverty, with help targeted at those who need it most, whether this be through a social tariff, support for those on pre-pay meters or other direct policies. Of course, a reduction in the demand side with funding for housing insultation and smart meters could also help to lower bills.