In the last few months, we have seen a substantial number of high price intervals in Queensland. Increased Market Demand on 9 March and the simultaneous trip of Gladstone units 3 and 4 on 31 March spiked energy prices to $8,800/MWh and $15,100/MWh levels, respectively. These price spikes occurred between 5pm and 7pm when the share of solar generation was only around 4% of its total daily output. How did these events affect solar revenue?

In this Chart of the week, Andrey Kotov examines how energy contingency events, such as coal units tripping and/or increased market demand, can increase the revenue of large-scale solar based on Q1 2022 observations. Of course, this is still only for a small portion of the time and is not necessarily a daily pattern that solar operators can take advantage of regularly; however, the ability of solar to capture at least some portion of evening peak pricing will be key to its continued long term profitability as midday prices continue to remain low and evening peak prices are expected to become more volatile, which could continue the trend of very low % of solar generation driving very high proportions of total revenue leaving solar project revenues at risk depending on changes to the timing of the evening peak.

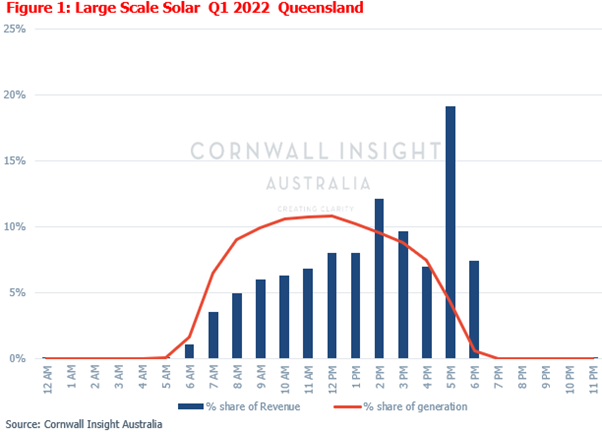

As shown in Figure 1, almost 27% of total Q1 2022 quarterly solar farm revenue in Queensland is earned from less than 5% of quarterly energy generation, in only two hours between 5pm and 7pm, suggesting extreme price events (>$10,000/MWh) pushing solar revenue up during this time interval. For Q1 2022, there were 60 5-minute intervals when prices spiked above the $10,000/MWh level between 5pm and 8pm. Assuming the solar farm is not constrained due to the grid stability reasons or any maintenance plans, the last few hours before sunset had the most value of all the hours examined in this analysis.

Despite Queensland prices in Q1 2022 averaging $149/MWh, captured prices for solar farms as a proportion of the average Q1 2022 prices were lower and averaged $117/MWh. While this is partially driven by unplanned coal outages and increased market demand in March 2022, it also fundamentally reflects growing daily volatility, especially during summer with evening periods becoming increasingly more valuable.

Going forward, whilst market fundamentals and economics will continue to determine the value spread of intraday pricing and volatility, solar farms will continue to realise a disproportionate revenue benefit (as a % of overall generation) from evening peak pricing events when they occur. Market players with flexible portfolios (solar and co-located battery storage) will have more options to capture price spikes through energy shifting or FCAS markets. For those market players that are 1-2 solar hours behind other competitors (further west of the east coast, like South Australia), their geographical location will likely be of additional benefit, as those assets will likely have higher generation volume and be able to better capture those evening peaks.

Cornwall Insight Australia’s in-house Benchmark power curve price forecast subscription services shed light on how prices are likely to evolve, considering the impacts of new regulations. For more information, please contact us at enquiries@cornwall-insight.com.au.