The government has released the budget and reference prices, along with the auction parameters, for the upcoming Contract for Difference (CfD) Allocation Round 6 (AR6). As recently reported, there were considerable questions outstanding about the parameters which will be used in the auction and significant pressure was placed on AR6 to be successful given shortcomings in last years AR5, in which no offshore wind assets won a contract. In this blog, we unpack the details of the recent announcement, and discuss the implications for the auction.

Budget:

The budget impacts competitiveness in the auction and the capacity of assets which can be awarded contracts, and so is crucial for the overall success of an Allocation Round.

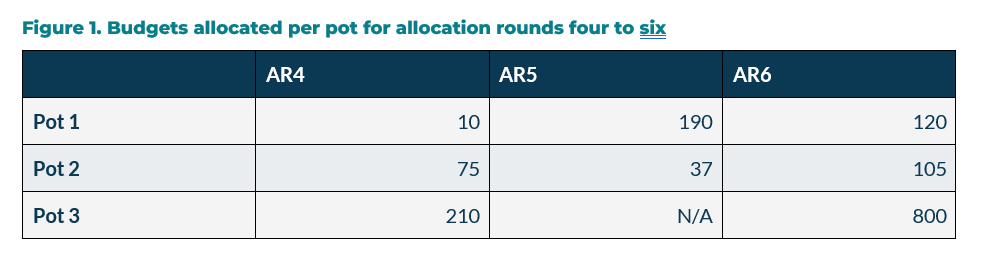

The budget released by the government sees a considerable increase from previous allocation rounds. The lack of engagement in AR5 by offshore wind assets appears to have impacted thinking, with £0.8bn/annum distributed into the standalone Pot 3 containing offshore wind. This is over four times the budget applicable for offshore wind assets last year, in which they had to compete not only with other offshore wind assets, but other technologies including solar and onshore wind after being transferred into Pot 1.

Onshore wind and solar assets technically see a reduction in budget from the £190mn/annum applicable last year, but this figure can be considered misleading. As discussed, a large portion of the budget last year was expected to be utilized by offshore wind assets. When compared to the budget for Pot 1 when offshore wind was not included in AR4, we see a considerable increase, moving from £10mn/annum to £120mn/annum (Figure 1).

Pot 2 also sees considerable increase, with a budget ~3 times higher than that seen last year.

Maxima/Minima

Maxima and minima are used by the government to control part of the budgets in specific pots; they can limit the maximum budget achieved by specific assets, or set minimum shares of the budget which can go towards specific technologies despite them being less competitive in the overall pot. In the budget notice, the government has indicated that maxima and/or minima will be applicable for all pots including:

Three separate maxima, each totalling £120 million, will be applied to Onshore Wind, Remote Island Wind and Solar PV in Pot 1. A Minimum of £10 million will be applied in respect of Tidal Stream in Pot 2. In addition, a Maximum of £8 million will be applied to Geothermal in Pot 2. Two separate Maxima, each totalling £800 million, will be applied to Offshore Wind Permitted Reduction projects and new Offshore Wind projects in Pot 3. In the supporting documentation provided, Permitted Reduction assets are defined as projects “that formed part of projects awarded a CfD in a previous Allocation Round and where these projects have since gone through the Permitted Reduction process in the contract terms. This process has allowed projects to withdraw a maximum of 25% of their original total project capacity from their CfD contract and now use that reduced capacity to bid into AR6 as a standalone project“.

Reference prices

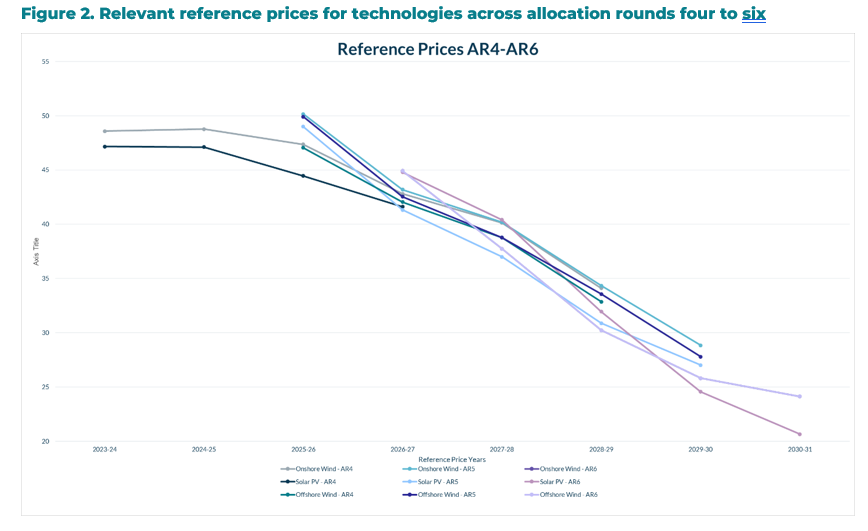

The reference prices are used in the auction as a proxy for future market prices, determining the overall cost of the scheme (based on the difference payment of the submitted bid price minus the reference price). The lower the reference price, the greater the overall cost per project and so the higher the impact on the budget.

The updated reference prices show a continued reduction over the relevant delivery years/modelled periods for assets, with the lowest prices being achieved in the final valuation year (2030-31), with the rates for offshore wind, onshore wind and solar assets being lower than lowest reference prices achieved in AR4 and AR5.

This is significant as it means that the cost per asset in these years will be significant, being more substantial that an asset bidding at the same price in previous allocation rounds. As a result, this mitigates some of the benefits of the high budget, creating uncertainty for market participants.

There can be mixed feelings in regards to the released data for AR6, and there are still some minor uncertainties which need clarifying, so approaches are subject to change, but the significant budget set aside for AR6 (combined with the high ASPs published previously) should provide a large amount of comfort to participants that viable deployed rates are achievable. However, the high level of reference prices will mean that competition is still likely to be fierce.

Cornwall Insight provides a wide variety of CfD services, including our new CfD Support Service, designed to provide detailed support to auction participants through the application and allocation round process.

If you would be interested in discussion these services in more detail, please contact a.asher@cornwall-insight.com

This blog was taken from our Industry Essentials service. If you are a subscriber, log in to your account on CATALYST to read the full blog.