Cornwall Insight has released its final forecast for the October–December 2025 Default Tariff Cap (price cap), following the closure of the observation window on 18 August1.

The new forecast predicts the cap will rise to £1,737 a year for a typical dual fuel household2 this winter. This would represent an increase of £17 and 1% from the current price cap which is set at £1,720 per year. Ofgem is scheduled to announce the official cap on 27 August.

This forecast reflects upcoming changes we have assumed Ofgem will be introducing in this cap period. This includes the expansion of the Warm Home Discount (WHD) scheme for vulnerable households that was announced by the government in June – adding around £15 to a typical bill, while also providing £150 in support to 2.7mn households. The forecast also includes other adjustments to the modelling of certain inputs for the cap. If policy decisions change, or new policies are introduced, the price cap is likely to change.

The wholesale prices for electricity and gas have been volatile over the observation window, largely reflecting geopolitical factors - with uncertainty over US trade policy remaining an underlying concern - as well as legislative developments from the European Union, but their general trend has been downwards.

While wholesale natural gas prices surged in mid-June with Israel’s airstrikes on Iran intensifying concerns over disruptions to liquefied natural gas (LNG) shipments, market sentiment subsequently eased, with prices falling back as a result. They have since continued to trade between the levels seen throughout most of the second quarter of the year.

Confirmation from the European Parliament that the rules on gas storage stocks for the winter months would be eased for member states also contributed to the decline in prices.

Looking ahead, we expect a small drop in the price cap in January. However, this is subject to geopolitical movement, weather patterns, changes to policy costs and the potential introduction of new policy costs such as those to support investment in new nuclear generating capacity.

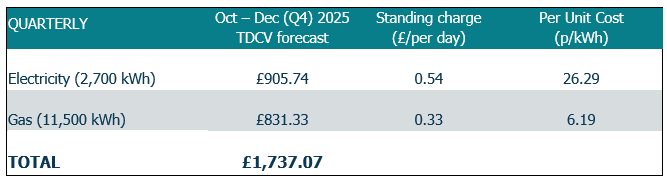

Figure 1: Cornwall Insight’s Default Tariff Cap forecast, Per Unit Costs and Standing Charge (dual fuel, direct debit customer)

Source: Cornwall Insight’s Default Tariff Cap Forecast Service

Dr Craig Lowrey, Principal Consultant at Cornwall Insight:

“News of higher bills will not be welcomed by households, especially as winter approaches. While the added costs behind this forecasted rise are aimed at supporting those most in need, it does mean typical bills will increase despite relatively lower wholesale costs. It’s a reminder that the price cap reflects more than just the market price of energy.

“This immediate challenge underscores a broader uncertainty facing millions of households, with current forecasts suggesting a sharp drop in bills is unlikely in the near term. Longer term, Ofgem's review of how Britain's energy system costs are distributed could reshape the financial burden on consumers, but while some may see savings, others could face higher charges.

“The real hope for lasting relief lies in the longer-term transition towards clean power and energy independence, which offers the greatest prospect of both stability and lower costs. But there’s no sugarcoating it, this transition won’t be instant or effortless and will see costs incurred as a result. It will require adaptation and significant upfront investment - every change in the energy landscape comes with trade-offs. Yet for all the challenges, the long-term reward could be a more sustainable and affordable energy system for generations to come.”

Reference:

1. The period of time Ofgem use to monitor the market and calculate the wholesale element of the cap.

2. Ofgem’s Typical Domestic Consumption Values (TDCVs), are set at 2,700 kWh per annum for electricity, and 11,500 kWh per annum for gas.

Notes to Editors

For more information, please contact: Verity Sinclair at v.sinclair@cornwall-insight.com

To link to our website, please use: https://www.cornwall-insight.com/

Copyright disclaimer for commercial use of the press releases:

The content of the press release, including but not limited to text, data, images, and graphics, is the sole property of Cornwall Insight and is protected by UK copyright law. Any redistribution or reproduction of part or all of the content in any form for commercial use is prohibited without the prior written consent of Cornwall Insight.

Media Use Exemption:

The information included in this press release may be used by members of the media for news reporting purposes only. Any other commercial use of this information is prohibited without the prior written consent of Cornwall Insight.

All non-media use is prohibited, including redistribution, reproduction, or modification of our content in any form for commercial purposes, and requires prior written consent. Please contact: enquiries@cornwall-insight.com

About the Cornwall Insight Group

Cornwall Insight is a leading provider of research, analysis, consulting and training to businesses and stakeholders engaged in the Great British and Irish energy markets. To support our customers, we leverage a powerful combination of analytical capability, a detailed appreciation of regulation codes and policy frameworks, and a practical understanding of how markets function