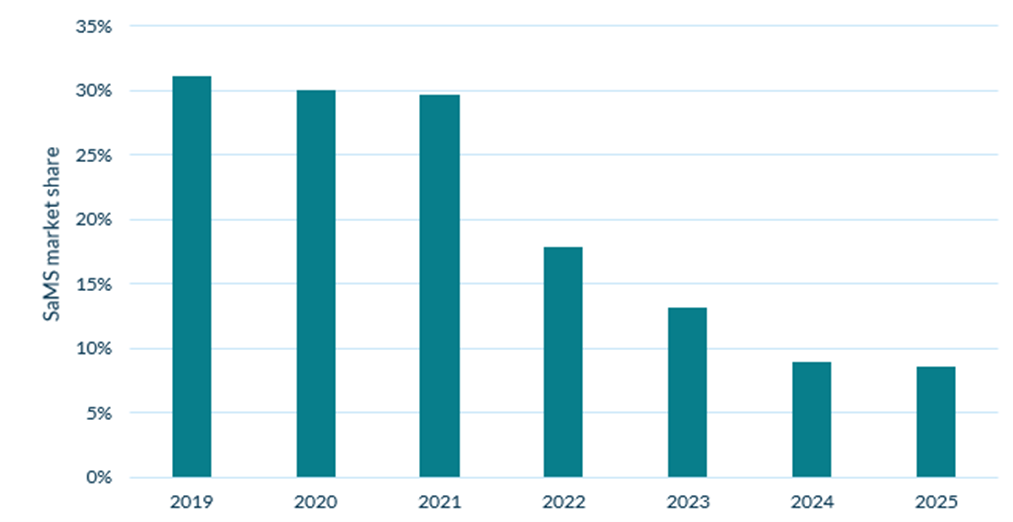

The share of the domestic energy market held by small and medium-sized suppliers (SaMS) fell to just 8.6% in the second quarter of 2025, down from 8.9% in the previous quarter, according to Cornwall Insight’s Domestic Market Share Survey.

Great Britain’s six largest suppliers now account for 91.3% of the domestic market, a significant change from the landscape before the energy crisis, where at their peak SaMS held over 31% of the market.

The fall from Q125 to Q225 reflects British Gas taking on 84,000 customers from Rebel Energy through the Supplier of Last Resort process, alongside updated customer figures for other SaMS.

The trend towards consolidation has been evident for many years and is largely due to the fallout from the energy crisis, which saw 26 domestic suppliers exit the market. All these suppliers, with the exception of Bulb, were in the small and medium category. Whilst larger suppliers had the financial resources to manage extreme wholesale price volatility, smaller providers did not have the capital, meaning many exited the market.

Even though market conditions have improved since the height of the crisis, profitability is still tight, particularly for smaller suppliers. High wholesale prices continue to be a challenge, and new regulatory requirements from Ofgem are adding extra pressure, especially for suppliers without dedicated regulatory teams.

New entrants into the market have also slowed significantly. Since 2021, just three suppliers have entered the domestic market, a sharp contrast to 2017, in which there were 17 new entries in a single year. While it’s unclear if the market will return to that level of competition, current conditions suggest consolidation is set to continue for now.

Figure 1: Small & Medium Energy Supplier Market Share Over Time

Source: Cornwall Insight

Matthew Smith, Analyst at Cornwall Insight said:

“We’re continuing to see the effects of the energy crisis play out in the domestic market. The numbers show a continued shift away from a highly competitive, fragmented supplier base towards a more consolidated market dominated by the biggest players.

“With wholesale prices staying comparatively high compared to pre-crisis levels, and new regulatory responsibilities coming in, it’s tough for smaller suppliers to grow, or for more to enter the market. If wholesale prices fall, we may see a return of small and medium sized suppliers, but under current conditions, all signs point to a continued reduction in their market share.”

Reference:

1. The Six largest suppliers are: British Gas, E.ON Next, EDF, Octopus Energy, OVO and Scottish Power

Find out more about our Supplier Insight Service here and request a demo of here.