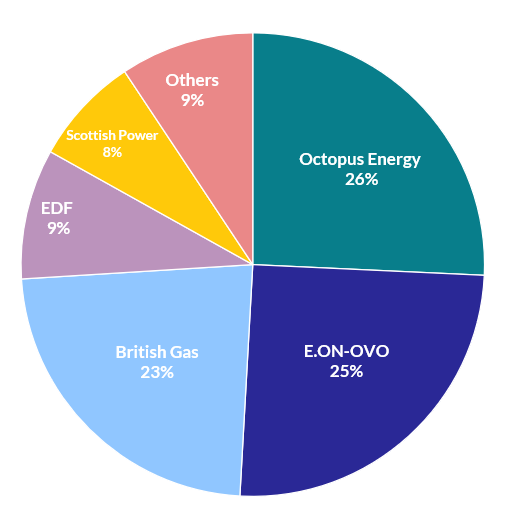

E.ON’s acquisition of OVO would make it the second largest domestic supplier in Great Britain, with around 25% of the market, just behind Octopus Energy at 26%, according to Cornwall Insight’s Domestic Market Share Survey.

Since 2020, a combination of sustained high wholesale prices and increased regulatory requirements has led to the exit of many smaller suppliers. Six energy companies currently hold over 90% of the household energy market, this will reduce to five if the transaction is approved. The three largest suppliers would together account for close to three quarters of total market share.

High wholesale energy prices, coupled with the price cap, have also lowered the number of households switching their energy supplier. Switching levels remain significantly below pre-2020, resulting in the market being less attractive to new entrants.

Domestic market share can be measured in different ways. Cornwall Insight measures market share by the total number of electricity and gas accounts a supplier has on live supply, this means dual fuel consumers who receive both gas and electricity are counted as two accounts. By contrast, if measuring by the number of customer accounts, then a dual fuel customer is only counted once, regardless of how many fuels are supplied. This is why supplier rankings may differ depending on the metric being used.

Energy accounts are generally considered a more meaningful measure of supplier scale within the domestic energy market because they better reflect the number of supply points being served and the overall size of a supplier’s retail portfolio.

Figure 1: Domestic Energy Market Share following E.ON’s acquisition of OVO Energy

Source: Cornwall Insight Domestic Market Share Survey

Tom Goswell, Energy Supply Lead at Cornwall Insight:

“The proposed deal reflects a market that has changed significantly over the past five years. Higher costs and tighter regulation have naturally favoured suppliers with the scale to absorb them, and E.ON acquiring OVO is a logical step in that direction.

“Larger suppliers can bring stability, resilience, and the ability to invest in the products and services that will matter as households move towards heat pumps, EVs, and flexible tariffs. However, as the market becomes more concentrated, it will be important to consider what this means for consumer choice. The conversation for policymakers is making sure that consolidation and competition aren’t mutually exclusive, because households will need both stability and choice as the market evolves.”

The conversation for policymakers is making sure that consolidation and competition aren’t mutually exclusive, because households will need both stability and choice as the market evolves.

Tom Goswell

Energy Supply Lead at Cornwall Insight

Energy Supply Market Intelligence

Data and intelligence covering energy suppliers and third-party intermediaries, including proprietary market share data, pricing analysis and financial information. This helps energy suppliers understand the competitive landscape, navigate risks, identify opportunities, and make informed strategic decisions.