Energy bills are forecast to rise by £209 to £1,850 a year for a typical dual fuel household1 from July, according to Cornwall Insight’s final forecast for the July – September 2026 Default Tariff Cap (price cap), released following the close of the observation window2 on 18 May.

The new cap would represent an increase of 13% on the current £1,641 annual bill.

The main driver for the increase in our forecast is rising wholesale prices, which climbed sharply in February and March after US and Israeli missile strikes on Iran, and the subsequent retaliatory attacks, saw damage to Gulf energy infrastructure and the closure of the Strait of Hormuz, a shipping route for around 20% of global oil and gas. A temporary ceasefire brought some calm to markets, but prices remained elevated throughout the observation window, pushing the July forecast to more than £200 above the current cap.

While households will be understandably frustrated by a rise during the summer, the impact will be reduced as household energy usage typical falls during the hotter months. The bigger concern is October, when demand picks up again and current forecasts point to a similar cap level as July. While the October cap will depend on how the Middle East conflict unfolds, even if the conflict were to end tomorrow, the physical damage to infrastructure, and lingering effect of disrupted supply, means a fall back to April’s price cap levels in the autumn looks unlikely.

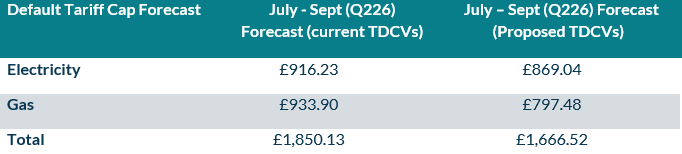

Separately, Ofgem is consulting on a change to its definition of an ‘average household’, known as typical domestic consumption values, to reflect the fact that average household energy use has fallen3. The energy regulator regularly undertakes such reviews, the last one being in 2023, with Ofgem stating that it is minded to adopt these lower numbers for inclusion in its cap methodology from July 2026 at the earliest.

Cornwall Insight has therefore published two forecasts. If Ofgem adopts the lower consumption figures, the headline “average bill” could appear to rise by less. However, as the cap controls unit rates and standing charges, rather than the total bill itself, what households actually pay will depend on how much energy they use and will not be impacted by Ofgem’s “average bill” figure.

Figure 1: Cornwall Insight’s Default Tariff Cap forecast (dual fuel, direct debit customer)

Source: Cornwall Insight’s Default Tariff Cap Forecast Service

Figure 2: Default Tariff Cap forecast, Per Unit Costs and Standing Charge (dual fuel, direct debit customer). These do not include the variances above.

Source: Cornwall Insight’s Default Tariff Cap Forecast Service

Note: All figures are national average unless otherwise stated. All intermediate and final calculations are rounded to two decimal places. Totals may not add due to rounding.

Dr Craig Lowrey, Principal Consultant at Cornwall Insight:

“Over the past few months, we’ve watched our forecasts shift from showing virtually no quarter-on-quarter increase to a 13% rise in current bills – with this change due to the impacts of the Middle East conflict. A summer rise will be painful for households, but the bigger concern is October when household demand traditionally picks up. If the cap stays at a similar level as July, that is when the Government will need to think seriously about targeted support for the most vulnerable.

“As a net importer of liquefied natural gas, global price shocks have hit us hard, and that vulnerability isn’t going away.

“Short-term support can protect the most vulnerable households, but it won’t address the underlying problem. While Government’s plans, such as proposals to decouple electricity prices from gas, are well-intentioned, and in time they could make a small difference, gas is still likely to set the price the majority of the time, so consumers won’t feel a substantial change. Building out our renewable capacity is the only real path to bills that aren’t as exposed to events thousands of miles away. It won’t be cheap, and bills will not see an immediate drop, but that is the direction of travel if we want genuine, lasting stability.”

Reference:

- The period of time Ofgem use to monitor the market and calculate the wholesale element of the cap.

- Ofgem’s central case Typical Domestic Consumption Values (TDCVs) are currently set at 2,700 kWh per annum for electricity and 11,500 kWh per annum for gas.

- Ofgem may reduce its central case Typical Domestic Consumption Values (TDCVs) to 2,500 kWh per annum for electricity and 9,500 kWh per annum for gas.

A summer rise will be painful for households, but the bigger concern is October when household demand traditionally picks up. If the cap stays at a similar level as July, that is when the Government will need to think seriously about targeted support for the most vulnerable.

Dr Craig Lowrey

Principal Consultant at Cornwall Insight

Default Tariff Cap Predictor

Our Default Tariff Cap Predictor forecasts Ofgem’s quarterly price cap and examines the key drivers affecting the level of the cap, and – in turn – household energy bills.