Ofgem has announced the July Default Tariff Cap (price cap) at £1,862 per year for a typical dual fuel household1, up £221 or 13% on current levels. While this is unwelcome news for billpayers, for many, the more pressing concern will be what follows. Cornwall Insight’s first forecast for October to December puts the cap at £1,899 per year, this would represent a 2% rise on July’s cap, that would come in just as temperatures fall and energy usage rises.

The October figure will not be confirmed until August, and there remains a lot of time for wholesale market conditions to shift. However, the direction of travel is being shaped by several unknowns that are unlikely to be resolved quickly.

Wholesale energy prices, which account for over 40% of the cap, climbed sharply earlier this year with the conflict in the Middle East. While wholesale prices have since declined from the levels seen in March, they remain well above where they were before the conflict began. The Strait of Hormuz remains closed, infrastructure damage will continue to impact oil and gas production, and the effects on global supply chains and market confidence are ultimately feeding through to what households pay.

In addition to the cap announcement, Ofgem has said from 1st July it will change how it defines the average household2, known as the Typical Domestic Consumption Values (TDCVs), reflecting the fact that typical energy consumption has fallen in recent years.

Under the new TDCVs the cap will rise to £1,663 per year for a typical household, and under the current TDCVs it will rise to £1,862 per year.

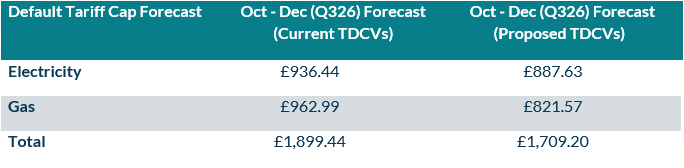

Cornwall Insight has modelled the October cap under the current TDCVs and the TDCVs that are due to come in from July . Under the new consumption values, the October cap forecast stands at £1,709 per year, compared to £1,899 under the current definition. It is worth noting that the cap itself controls unit rates and standing charges, not total bills, so what households actually pay will depend on how much energy they use.

The forecast for October will likely increase calls for the Government to lay out its plans for energy bill support over the winter if prices remain elevated over the coming months. They have already confirmed that if any support is provided then this will be targeted, unlike the universal support provided following Russia’s invasion of Ukraine. However, if the government do decide to implement support, the way in which eligibility for this support will be determined, as well as the way in which the scheme will be administered, has not been announced. Longer term measures to bring down bills – including cutting the country’s reliance on gas imports whose prices remain highly volatile – have also been the subject of debate, with the conflict in the Middle East keeping energy security at the top of the agenda.

Figure 1: Cornwall Insight’s Default Tariff Cap forecast (dual fuel, direct debit customer)

Source: Cornwall Insight’s Default Tariff Cap Forecast Service

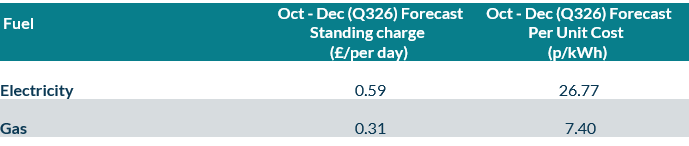

Figure 2: Default Tariff Cap forecast, Per Unit Costs and Standing Charge (dual fuel, direct debit customer). These do not include the variances above.

Source: Cornwall Insight’s Default Tariff Cap Forecast Service

Note: All figures are national average unless otherwise stated. All intermediate and final calculations are rounded to two decimal places. Totals may not add due to rounding.

Dr Craig Lowrey, Principal Consultant at Cornwall Insight:

“The rise in July energy prices will be felt across households already stretched by the cost of living, and even though it was widely anticipated, that does not make it any easier to bear. Even more concerning is October, where our forecasts are already pointing to a further rise landing just as people start to turn their heating back on for winter.

“A lot of people assume that if the conflict in the Middle East ended tomorrow, prices would return to their pre-conflict levels fairly quickly. However, that may be overly optimistic. The damage to infrastructure, the disruption to supply chains and the erosion of market confidence will not unwind overnight, and the impacts could be felt in bills for longer than many expect.

“That uncertainty makes the outlook for October particularly hard to call. We are only days into the three month time period Ofgem uses to set the wholesale element of the October cap, so things can and likely will shift, but households should not be banking on lower bills later in the year. The Government will face real pressure to spell out what support is available – and to whom – before winter. For a lot of people this is not some abstract economic question, it is a decision about how warm they can afford to keep their home.

“What we do know is while some form of short-term support will be needed, without a longer-term move away from energy imports, whose prices can shift dramatically, we are going to keep having this conversation.”

Reference:

- Ofgem’s central case Typical Domestic Consumption Values (TDCVs) are currently set at 2,700 kWh per annum for electricity and 11,500 kWh per annum for gas.

- New Typical Domestic Consumption Values (TDCVs) coming in from 1st July – 2,500 kWh per annum for electricity and 9,500 kWh per annum for gas.

A lot of people assume that if the conflict in the Middle East ended tomorrow, prices would return to their pre-conflict levels fairly quickly. However, that may be overly optimistic.

Dr Craig Lowrey

Principal Consultant at Cornwall Insight

Default Tariff Cap Predictor

Our Default Tariff Cap Predictor forecasts Ofgem’s quarterly price cap and examines the key drivers affecting the level of the cap, and – in turn – household energy bills.