The GB energy market powers millions of homes and businesses, yet many people working in the sector only see one part of how it operates. From generators and suppliers to network operators and regulators, a wide range of organisations work together to keep energy flowing across Great Britain. With ongoing market reform, a growing focus on decarbonisation and more professionals entering the sector, now is a good time to revisit the fundamentals of the GB energy markets.

What are the GB Gas and Electricity Markets?

The markets are often used as shorthand to refer to the system through which electricity and gas are produced, traded, transported, and ultimately supplied to homes and businesses across Great Britain. It is one of the most mature liberalised energy markets in the world, having been shaped by privatisation starting in the 1980s.

At its core, the market is designed to encourage competition. Energy suppliers compete to offer the best value and service to consumers, while wholesale energy markets enable the buying and selling of electricity generation and gas. Alongside this, regulated transmission networks and distribution networks ensure energy is safely and reliably delivered to customers.

The system operates within a comprehensive regulatory framework overseen by Ofgem, which sets rules, monitors competition, and protects consumers, while newer institutions like the National Energy System Operator (NESO) play an increasingly important role in system coordination and future planning.

Who are the Key Participants in the GB Energy Markets?

1. Generators (Electricity generation)

Electricity generators produce power from a range of sources, including gas, nuclear, wind, solar, and other renewables. Over time, the mix has shifted significantly towards low-carbon electricity generation, driven by policy and investment in renewable, to the point where low-carbon generation accounted for over 60% of all generation in the last year.

There are many companies that own and operate existing power stations and continue to invest in new assets, including large Pan-European companies such as E.On, Statkraft, EDF Energy, and Ørsted, but also companies that specialise in specific technologies including Octopus Energy Generation and Renewables Energy Systems (RES), to name a few.

2. Gas producers

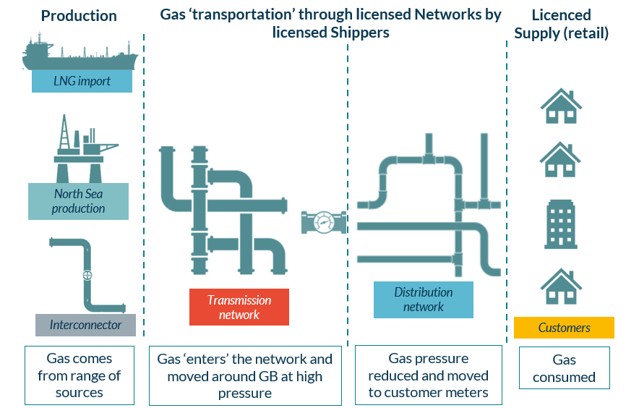

Gas producers extract natural gas from domestic sources (such as the UK Continental Shelf) or import it via pipelines and liquefied natural gas (LNG). This gas feeds both heating demand and gas-fired electricity generation. Key import terminals for LNG cargoes are the Grain LNG Terminal in Kent, and the South Hook LNG Terminal and Dragon LNG in Pembrokeshire, Wales.

3. Energy suppliers

Energy suppliers are the companies most visible to consumers. They purchase electricity and gas in the wholesale energy markets and sell it to households and businesses. Suppliers manage billing, customer service, and tariffs, and operate in a competitive retail market. There are around 20 suppliers selling to households, with the five largest by market share being Octopus Energy, EDF Energy, E.On UK, Scottish Power and British Gas. There are around 60 suppliers selling to businesses, including some of the companies that sell to households but also others including Corona Energy, SEFE and Total Energies.

4. Traders and wholesale markets

Energy trading takes place in wholesale energy markets, where electricity and gas are bought and sold ahead of delivery. Traders manage risk by purchasing or selling the forecast amount of gas or electricity that will ultimately be consumed by customers and help ensure liquidity in the market. Prices formed here ultimately influence what consumers pay.

5. Transmission network operators

Transmission networks transport electricity and gas over long distances at high voltage (electricity) or high pressure (gas). The electricity transmission networks are owned by National Grid Electricity Transmission, Scottish Power Transmission, and SSE Networks Transmission. There is a single owner, National Gas, of the gas transmission network.

These networks connect large generators, gas import points, and major demand centres. They are natural monopolies and are therefore regulated to ensure reasonable charges for those that use the networks.

6. Distribution network operators

Distribution networks deliver electricity and gas from the transmission systems to homes and businesses. Like transmission networks, they are regulated monopolies and play a critical role in maintaining local supply reliability. There are several owners, including UK Power Networks, Northern Power Grid in electricity and in gas companies include Cadent and Northern Gas Networks.

7. Ofgem

Ofgem is the independent regulator for the GB energy market. It oversees market rules, sets price controls for networks, protects consumers, and promotes competition.

8. NESO (National Energy System Operator)

NESO is responsible for coordinating the electricity system in real time, ensuring supply and demand are balanced. Its role is evolving as the energy system becomes more complex, particularly with the growth of intermittent renewable generation where output from, for example wind farms, is less predictable than gas fired power stations. It is also the key reason for the large increase in Battery Energy Storage Systems (BESS), where assets can compete for revenue to help NESO manage the electricity system in real time.

9. National Gas

In addition to being the owner of the gas transmission system, National Gas is also the System Operator for the gas network, ensuring that the supply of and demand for gas within the pipelines satisfies engineering operational requirements.

How Energy Moves Through the Value Chain

The GB energy market can be understood as a value chain:

- Production – Electricity generation and gas production create the energy supply.

- Trading – Energy is bought and sold in wholesale energy markets, ahead of real-time delivery.

- Transmission – Energy is transported across high-capacity networks over long distances.

- Distribution – Local networks deliver energy to end users.

- Supply – Energy suppliers sell electricity and gas to customers and manage the customer relationship.

While this flow appears linear, the reality is more dynamic. Energy trading happens continuously, system balancing occurs in near real time, and policy mechanisms influence behaviour at every stage.

Why the GB Energy Market has Become More Complex

Although the principle of liberalisation remains—competition driving efficiency and innovation—the market has become significantly more complex in recent years.

Several factors explain this:

- Energy transition and decarbonisation

The shift to low-carbon electricity generation has introduced new technologies such as wind and solar, which are intermittent and require more sophisticated system balancing. The rise of electric vehicles, heat pumps, and battery storage energy systems (BESS) is also changing consumption patterns and fuelling the rise of consumer-led flexibility markets. - Flexibility and system services

The rise of battery storage, demand-side response, and flexibility markets has added new layers to energy trading and system operation. - Market reform and policy evolution

Government and regulatory interventions—ranging from Contracts for Difference (CfDs) to capacity markets and retail price controls—have created additional mechanisms within the market. - Changing role of networks and system operators

Transmission networks and distribution networks are becoming more active participants in enabling flexibility and supporting decentralised generation.

Together, these developments mean that understanding how different parts of the GB energy market interact is more important—and more challenging—than ever.

Why Understanding the Wider Market Matters

For professionals working in the GB energy markets, having a broad understanding of the full value chain can be highly valuable.

Whether you work in:

- Sales or marketing, where customer propositions depend on wholesale prices and competition,

- Finance or pricing, where costs are shaped by trading, network charges, and policy,

- Customer operations, where regulatory requirements and supplier obligations are key,

- Trading or risk, where market dynamics and system conditions drive decisions,

…understanding how the system fits together helps provide context.

It enables better decision-making, improves cross-functional collaboration, and builds confidence when engaging with stakeholders across the sector. In a market defined by change, this broader perspective is increasingly essential.

Taking the Next Step: Deepening your Understanding

For those looking to build or refresh their knowledge of the GB energy market, structured learning can provide a faster, more coherent route than trying to piece together information from multiple sources.

Cornwall Insight’s CPD-accredited Introduction to GB Energy Markets course is designed to give a clear, end-to-end overview of the sector. Delivered online by industry experts, it covers:

- Consumer markets and energy suppliers

- Wholesale energy markets and energy trading

- Transmission networks and distribution networks

- Policy, regulation, Ofgem, NESO, and the energy transition

The course is delivered in four focused sessions and is regularly updated to reflect changes in the GB energy markets.

For anyone entering the sector—or looking to broaden their perspective—grasping these fundamentals is a critical first step.

Our next live course delivery dates:

14 – 17 July 2026 | 10am – 12pm

18 – 21 August 2026 | 10am -12pm

For more information about this course please contact Tom Davidson, Head of Learning Solutions, at: t.davidson@cornwall-insight.com

-

Introduction to the GB Energy Markets Academy

Discover more: Introduction to the GB Energy Markets AcademyEssential training for anyone new to the GB energy markets, delivered live or on-demand