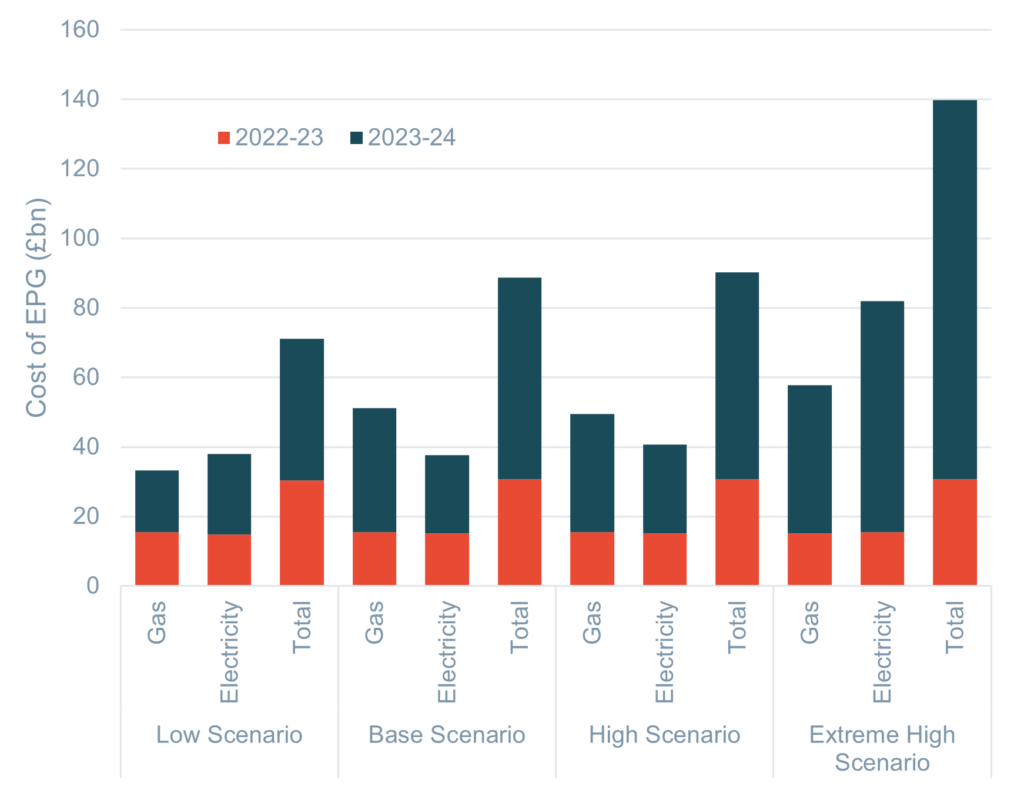

Modelling from Cornwall Insight has forecast the two-year cost of the Energy Price Guarantee (EPG) to be between £72bn in the lowest case scenario, and £140bn in the extreme high case scenario1. The data included in our new EPG report ‘Counting the Costs’, shows a near doubling of the forecasts between the best and worst cases – serving to highlight the extent of uncertainty relating to the cost of the scheme.

Factors such as energy demand, weather, geo-political uncertainty, global LNG prices as Europe looks to refill gas storage next summer, performance of European electricity and gas infrastructure, further policy and regulatory intervention, and the actions of hostile and unpredictable actors are all highly uncertain over the two-year period of support, and most are outside the government’s control.

The domestic EPG involves the government funding suppliers to cap the unit price for wholesale power and gas and removes the policy costs of green levies from household bills for a period of two years. Whilst this delivers unit price certainty and lower bills to households than otherwise would have been the case, it leaves government exposed to electricity and gas prices in unpredictable global commodity markets. Through Cornwall Insight’s modelling and quantitative analysis, we identified the difference between the EPG price levels and the forecasted actual costs of energy for consumers over four plausible different energy market scenarios. These scenarios are based on a mix of recent market price expectations and our own fundamental models.

The figures lay out the significant potential financial impact of the scheme in all scenarios, and the difficult task the government will have in scaling the true financial impact as it manages the wider economy.

Figure 1: Table of the EPG costs under the different Cornwall Insight scenarios

| £bn | 2022-23 | 2023-24 | TOTAL |

| Market Base (using 28-Sept-2022 energy prices) | 30.74 | 58.05 | 88.79 |

| Low | 30.74 | 40.87 | 71.61 |

| High | 30.74 | 59.41 | 90.15 |

| Extreme High | 30.74 | 109.10 | 139.84 |

Source: Cornwall Insight

* Using an estimated 29mn households in the UK and Ofgem’s annual Typical Domestic Consumption Value of 12,000kWh gas and 2,900kWh for electricity

Figure 2: Graph of the EPG costs under different scenarios

Source: Cornwall Insight

* Using an estimated 29mn households in the UK and Ofgem’s annual Typical Domestic Consumption Value of 12,000kWh gas and 2,900kWh for electricity

Gareth Miller, CEO, at Cornwall Insight:

“While the modelled costs of the EPG across all our market scenarios are clearly large, it is the significant variation in forecasts which jumps out of our report. There is nearly £70bn difference between the Low and Extreme High market scenarios. This reflects a febrile wholesale market continuing to be beset by geopolitical instability, sensitivity to demand, weather, and infrastructure resilience. The risk around these factors grows in the second year of the scheme as uncertainty increases with time. No one is clear on what the single curve of prices will be, so the government will find it hard to accurately plan for how to cover the EPG expenditure

“Fortune befriends the bold, but it also favours the prepared. The large uncertainties around commodity markets over the next two years means that the government could get lucky with costs coming out at the low end of the range, but the opposite could also be true. In each case, the government may find itself passengers to circumstances outside its control, having made policy that is a hostage to surprises, events and volatile factors. That’s a difficult position to be in.

“The good news is that there is a route through this. The government could use the next few months to develop more targeted energy support policies for households, building on proposals brought forward during the late summer across industry actors and think tanks. At the time, the urgency of the imminent Default Tariff Cap cliff edge prompted a universal response by government due to its simplicity and speed. With that pressure now lifted, there is oxygen to breathe deeply and look at targeted support again. This could still be wide enough to recognise the impacts of the higher market energy costs on many households, but with the advantage of potentially lower costs overall, and affording a road-testing opportunity for more progressive and enduring ways of dealing with higher costs over the long term.

“Politically there doesn’t need to be a decision to migrate to these schemes right away. The government could set review points for the universal scheme to assess whether it should be continued or transitioned, working up and consulting on targeted options in the meantime. This is very similar to the approach they are taking on business energy support and recognises the wide range of possible price environments that could play out.

“Alongside this, there is the opportunity still to drive simple changes in behaviour to reduce energy demand, a lever that could and should be pulled now which could reduce the pressure on prices more broadly, helping both households and the public finances. This would also create some financial capacity to extend more sustainable support should markets not revert to pre-crisis prices after the two years is up, which is certainly what our fundamental energy price models suggest may happen.

“A week is a long time in politics as we have just observed, but two years is an age in commodity markets, armed conflict and geopolitics. In this environment, flexible and durable policies, with pressure valves and elastic coverage, will be more sustainable than rigid and universal ones.”

Reference:

- Summary of Cornwall Insight modelling scenarios :

Cornwall Insight have produced three scenarios, low, base, and high. Given the high levels of volatility.

We also included an “Extreme High” scenario this represents an assessment of costs based upon the highest recorded prices on the wholesale curve observed to date for the EPG period (26 August 2022). This shows a surge in the costs of the EPG to approximately £140bn.

In establishing these scenarios, we have used our wholesale price modelling of our Benchmark Power Curve, alongside our Third Party Charges (TPC, also referred to as non-energy costs) modelling, in conjunction with our assessment of the Default Tariff Cap. As confirmed by the government, the EPG will be set at a rate of 34.00 pence per kWh (inc. VAT) for electricity and 10.30 pence per kWh (inc. VAT) for gas.

| Case | Description |

| Base | Calculated Default Tariff Cap rates for Q422 and Q423 calculated as per Ofgem methodology and Cornwall Insight analysis Dual fuel direct debit customer with central case Typical Domestic Consumption Value (TDCV), i.e., 12,000kWh per annum for gas and 2,900kWh for electricity, assuming 29mn households Assessment uses wholesale energy closing prices on InterContinentalExchange (ICE) for NBP natural gas, Baseload electricity and Peakload electricity on 28 September 2022 Single, central TPC scenario across all three cases, noting non-commodity costs are not the most profound driver of costs in this environment |

| High | Calculated Default Tariff Cap rates for Q422 and Q423 calculated as per Ofgem methodology and Cornwall Insight analysis Dual fuel direct debit customer with central case TDCV, i.e., 12,000kWh per annum for gas and 2,900kWh for electricity, assuming 29mn households Assessment uses Cornwall Insight BPC High Case scenario published October 2022 Single, central TPC scenario across all three cases, noting non-commodity costs are not the most profound driver of costs in this environment |

| Low | Calculated Default Tariff Cap rates for Q422 and Q423 calculated as per Ofgem methodology and Cornwall Insight analysis Dual fuel direct debit customer with central case TDCV, i.e., 12,000kWh per annum for gas and 2,900kWh for electricity, assuming 29mn households Assessment uses Cornwall Insight BPC Low Case scenario published October 2022 Single, central TPC scenario across all three cases, noting non-commodity costs are not the most profound driver of costs in this environment |

–Ends

Notes to Editors

For more information, please contact: Verity Sinclair at v.sinclair@cornwall-insight.com

To link to our website, please use: https://www.cornwall-insight.com/

About Cornwall Insight Group

Cornwall Insight is the pre-eminent provider of research, analysis, consulting and training to businesses and stakeholders engaged in the Australian, Great British, and Irish energy markets. To support our customers, we leverage a powerful combination of analytical capability, a detailed appreciation of regulation codes and policy frameworks, and a practical understanding of how markets function.