The government announced the reinstatement of ‘Pot 1’ technologies – which includes onshore wind and solar PV – in the next Contracts for Difference (CfD) Allocation Round 4 (AR4) in 2021. Research from Cornwall Insight’s Renewable Pipeline tracker highlights how competitive the AR4 auction could be, especially between ‘Pot 1’ technologies.

Cornwall Insight’s calculations show that 13.0GW of our pipeline could potentially be eligible*. This is split between 5.5GW of ‘Pot 1’ technologies, 6GW of offshore wind and a smaller proportion of ~1.0GW for ‘Pot 2’ technologies, with a significant proportion being Remote Island Wind (RIW).

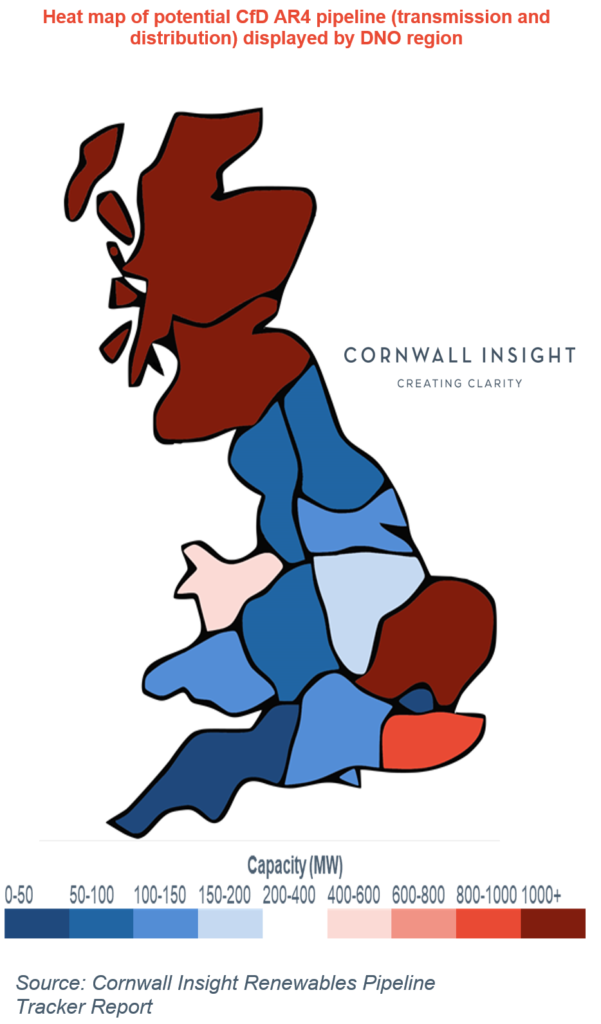

The heat map below shows the concentration of the potential successful projects. This indicates that of the potential CfD AR4 pipeline, a large majority is located in Scotland.

James Brabben Wholesale Manager at Cornwall Insight said:

“The results are revealing not just from a commercial perspective but on the interactions of wider policy and network charging.

“The onshore wind capacity totals 4.2GW, a high figure considering the ~13GW in operation currently. Of this, over 3.8GW is in Scotland, highlighting the continued concentration of sites here.

“Scotland is also home to all of the RIW pipeline, which totals 900MW. Dominating this is the potential 450MW Viking wind farm development on the Shetland Isles. With offshore wind carved into a separate ‘Pot 3’, RIW projects could be in a more competitive position when compared to previous auctions.

“Although the auction is set to be a competitive one, the location of potential applications may cause other issues such as high Transmission Network Use of System (TNUoS) costs for larger sites in Scotland, differences in load factors and site conditions and wider financing and strategic factors at play from project sponsors.

“The pipeline may also change as we head through to 2021. Particularly as some sites continue to look at subsidy-free and merchant options instead, while new sites may also join the queue for the CfD.”

–Ends

Notes to Editors

*This is calculated through:

- Filtering our calculated total pipeline of over 37GW across 800+ sites into those “most likely” to bid.

- These “most likely” are categorised as all CfD eligible technologies which have applied for or gained planning permission, or re-applied for and gained permission, post all subsidy scheme changes and closures. Effectively this is from early 2019 onwards.

- In our view these projects are most likely to be competitive in the auction, as prior to the recent BEIS announcements they would have been aiming to operate subsidy free anyway.

- A separate calculation is made for offshore wind, with all sites likely to be able to build by the delivery years of the next round, likely 2024 to 2026, included.

- From this, we use our database and wider data sources to place sites by their location against regions, specifically in relation to network connections.

- The differing scales of projects means there will be a mix of transmission and distribution connections, but our map groups these to align to the 14 distribution regions in order to visually display all of the data on one map.

- Concentrations in each zone therefore represent both larger transmission and smaller distribution connected sites, including offshore wind.