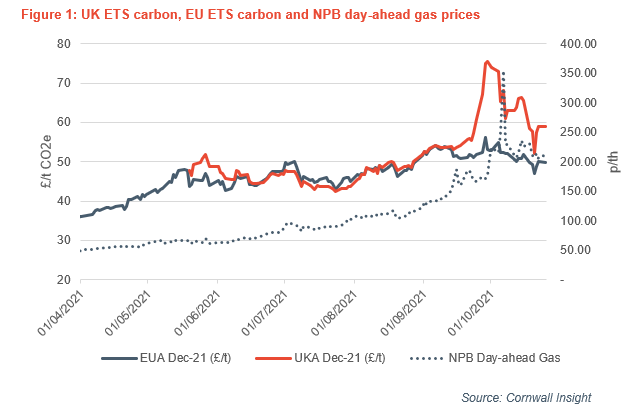

Cornwall Insight examines the first six months of the UK Emissions Trading Scheme (UK ETS), which launched on 19 May this year. The below graph shows the UK Allowance (UKA) Dec-21 futures contract since the scheme’s inception, alongside the EU Allowance (EUA) Dec-21 futures contract and National Balancing Point (NPB) day-ahead gas.

After enjoying an initial premium to the EU ETS, we saw UKA prices closely track its larger European cousin, with whom it shares an almost identical framework. Over May to August, the UKA price averaged £47.09/t, slightly above the EUA price of £46.20/t. From the 14 September, we began to see price divergence in the two carbon markets, with UKA prices continuing to rise alongside broader commodity markets (notably gas), while EUA prices eased to £51.00/t.

Price divergence peaked on 30 September, when UKA prices surged to a record £75.50/t, £14.05/t higher than the closing EUA price on the same day. With the added £18.00/t cost from the Carbon Price Support, the total carbon price for power generators on the day was over £93.00/t. Low wind generation and soaring gas prices have seen coal generators called upon more regularly and tightened the UK ETS market.

Luke Ansell, Analyst at Cornwall Insight, said:

“While UKAs continue to respond to movements in the gas market, EUA prices have seen a less strong correlation to gas contracts in recent weeks, despite increased demand from fossil plants, as seen in GB. Several factors may explain this: Firstly, near-curve European gas contracts are less relevant for the EUA price in terms of coal-to-gas fuel-switching dynamics at such high gas prices.

“Secondly, amid unprecedented gains in wholesale gas and power contracts, some commodities traders and utilities may be forced to sell their EUA positions to cover gas and power markets losses. Thirdly, there is growing speculation of policy intervention in the carbon market amid growing concerns from domestic and industrial consumers over high electricity prices. Fourth, the recent disruption of industrial activity, most notably for fertilizer manufacturers, has weighed on the demand sentiment.

“Divergence in the two markets is undoubtedly related to the immature nature of the UK ETS, which is a smaller scheme and therefore susceptible to greater volatility. In addition, unlike in the EU, UK installations have no previously accumulated surplus of allowances to draw upon in times of high demand, leading to a tighter supply-demand balance and greater volatility.

“If current UKA prices are sustained, we will see an injection of allowances into the UK ETS via the Cost Containment Mechanism (CCM), softening the supply-demand picture and putting some downward pressure on prices. The earliest opportunity for CCM intervention is now December if the monthly average UKA price exceeds the respective trigger price of £52.88/t across September, October and November.

“The monthly average in September was £57.84/t and is set to be even higher across October. However, prices have eased somewhat from the high’s seen in September, so it remains uncertain if we will see mechanisms under the CCM triggered.”

–Ends