Modelling from Cornwall Insight suggests European gas storage levels will end this winter between 45-61% full, with an average of 55% and could reach 88-100% full by September 2023. The data, included in our insight paper ‘Crisis behind, challenge ahead: European gas storage levels for 2023’ shows this would be at the high end of historical outcomes and compares to the previous end of winter record of 54% in 2020.

The level of gas storage in Europe at the end of winter will play a crucial role in determining whether Europe is past the worst of the energy crisis, or if 2023 will bring back high prices and supply concerns. Having higher storage levels at the end of this winter will mean less refilling is required to meet the EU targets before the 2023-24 winter, consequently improving the security of the energy supply.

However, there are a range of key variables that will influence how smooth the journey to refilling European storage will be ahead of next winter, as well as the price paid to procure sufficient gas to achieve adequate gas inventory refilling.

- Russian supplies: Maintaining the current levels of piped and liquid natural gas (LNG) supplies from Russia will be a key factor in our reliance on the global LNG market.

- East Asian demand: Chinese economic growth will likely have an impact on the global energy markets, but the extent of this impact currently remains uncertain.

- US exports: The US has been a crucial supplier of European LNG imports during the second half of 2022 but with increasing pressure to protect domestic consumers from electricity price hikes it remains to be seen if the commitment to supplying Europe with gas will waiver.

- Demand elasticity: Lower prices can be expected to increase demand if it benefits business and industrial profits, but the question remains whether alternate operating practices that have been adopted by companies in the meantime can compete economically with falling gas prices.

- Weather: Unseasonably warm weather over this winter helped to preserve gas storage levels, however, the lower snowfall will feed through into lower hydropower stocks and more dependence on gas during the summer. A warmer summer could also be a downside, with heatwaves triggering more energy demand for cooling, alongside further reducing water levels. Contrarily, a mild, windy, and wet spring and summer could act to reduce dependence on gas and support rapid refilling rates for European gas storage inventories.

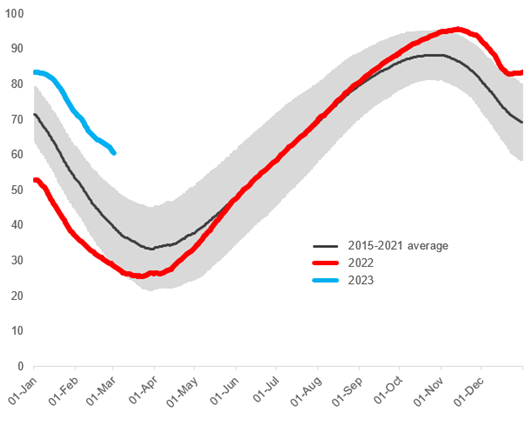

Figure 1: European gas storage levels (%) in 2022-23 (as of 2 March 2023) compared to the 2015-21 average and standard deviation range

Higher storage forecasts are unlikely to bring gas prices back to historic norms. Although storage in Europe can cover three months of winter demand, imports of expensive and volatile LNG will be needed to maintain inventory levels, replacing Russian pipeline gas. As a result, even with the optimistic outlook for storage levels, the price of gas in Europe will not drop to the previously recorded lows at the end of high storage-level winters.

Dr Matthew Chadwick, Lead Research Analyst at Cornwall Insight:

“Forecasts for European gas storage levels going into next winter are considerably more positive than they were last Autumn. As the risk of gas shortages falls, many may take this to mean Europe is past the peak of the energy crisis, but I would advise caution. Any single factor can influence the pace and pattern of storage refill, and perhaps more pertinently, change the cost paid to achieve it. We are certainly not out of the woods yet.

“What may ease this year is the heightened level of understandable panic that led to hectic energy-buying practices during the autumn of 2022. As a result, we can probably expect prices to be much more muted than 2022, despite any uncertainties that may come into play.

“Whatever the outlook for storage levels, the need to compensate for Russian pipeline volumes with expensive and volatile liquified natural gas will keep gas bills higher. This, at least for now, is the “new normal”, and consumers and economies should prepare for energy costs to remain higher than before the pandemic, and the Ukraine war, for some time to come.”

- Ends

Notes to Editors

For more information, please contact: Verity Sinclair at v.sinclair@cornwall-insight.com

To link to our website, please use: https://www.cornwall-insight.com/

About the Cornwall Insight Group

Cornwall Insight is the pre-eminent provider of research, analysis, consulting and training to businesses and stakeholders engaged in the Australian, Great British, and Irish energy markets. To support our customers, we leverage a powerful combination of analytical capability, a detailed appreciation of regulation codes and policy frameworks, and a practical understanding of how markets function.