Ahead of the July Default Tariff Cap (price cap) rise, Cornwall Insight has released new forecasts for October. The price cap is currently forecast to fall by 0.5% compared to July.

Our forecasts have eased slightly since May, with the US-Iran 60-day ceasefire, along with ongoing negotiations, helping to stabilise wholesale gas markets. However, conflicting reports on the reopening of the Strait of Hormuz, the patchy progress of peace talks, and uncertain repair timelines to key regional infrastructure mean prices remain high, if less volatile than in the Spring.

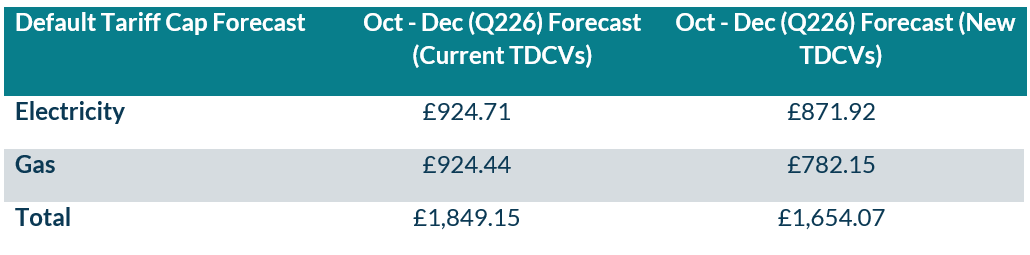

For a current typical household1, our forecast for October sits at £1,849 per year. Ofgem is updating its definition of a typical consumer from July2 to reflect falling household energy use, which adjusts the headline figure to £1,654 under the new values. On a like-for-like basis, that represents little change from July 20263.

The observation window4 is now at its midpoint. Elevated wholesale prices seen in May and parts of June will already be locked in, which means prices are unlikely to fall to the levels seen in the first three months of the year. The scale of any increase will depend on how long the geopolitical uncertainty continues.

While July’s higher prices will be cushioned by warmer weather and lower household energy use, the October cap lands as people switch their heating back on and will have a greater impact on household finances.

The government has several options available to support households during this time, and the new Prime Minister may be open to introducing targeted support for more vulnerable households if prices remain high.

Looking further ahead, we are currently forecasting a slight drop in the cap from January, but predictions remain above the bills seen during the first three months of the year.

Figure 1: Cornwall Insight’s Default Tariff Cap forecast (dual fuel, direct debit customer)

Source: Cornwall Insight’s Default Tariff Cap Forecast Service

Note:

- The new TDCVs come in from 1st July

- All figures are national average unless otherwise stated. All intermediate and final calculations are rounded to two decimal places. Totals may not add due to rounding.

Figure 2: Default Tariff Cap forecast, Per Unit Costs and Standing Charge (dual fuel, direct debit customer). These do not include the variances above.

Source: Cornwall Insight’s Default Tariff Cap Forecast Service

Dr Craig Lowrey, Principal Consultant at Cornwall Insight:

“The Iran ceasefire gave the markets some breathing room, but this is a pause, not a resolution to the conflict. What comes out of the final agreement, if there is one, will matter enormously for energy prices. And even in the best-case scenario, the enduring effects from the conflict will be with us for a while. Infrastructure takes time to repair, supply chains take time to recover, and households will be left dealing with the consequences for some time.

“October bills always hit harder than July’s because people are turning their heating on again, and this year that coincides with a difficult geopolitical backdrop. The new Prime Minister will face real pressure to act on support for vulnerable households, but the harder question is what comes after that, currently we are in a perpetual cycle of global shocks, high bills and short-term fixes.

“More permanent measures like social tariffs, moving levies into general taxation, or removing VAT on energy bills would take some of the pressure off bill-payers, but there is no firm steer that these options are being actively pursued by Government at the moment.”

Reference:

- Ofgem’s central case Typical Domestic Consumption Values (TDCVs) are currently set at 2,700 kWh per annum for electricity and 11,500 kWh per annum for gas.

- New Typical Domestic Consumption Values (TDCVs) coming in from 1st July – 2,500 kWh per annum for electricity and 9,500 kWh per annum for gas. The change reflects the fact that typical energy consumption has fallen in recent years.

- The price cap for July – September has been set by Ofgem at £1,862 under current TDCVs and £1,663 under the TDCVs coming in from 1st July.

- The period Ofgem uses to calculate the wholesale element of the cap.

The Iran ceasefire gave the markets some breathing room, but this is a pause, not a resolution to the conflict. What comes out of the final agreement, if there is one, will matter enormously for energy prices.

Dr Craig Lowrey

Principal Consultant at Cornwall Insight

Default Tariff Cap Predictor

Our Default Tariff Cap Predictor forecasts Ofgem’s quarterly price cap and examines the key drivers affecting the level of the cap, and – in turn – household energy bills.