Due to market volatility, world events and Ofgem’s new methodology, our price cap prediction has changed.

Please see the latest predictions via our blogs page here

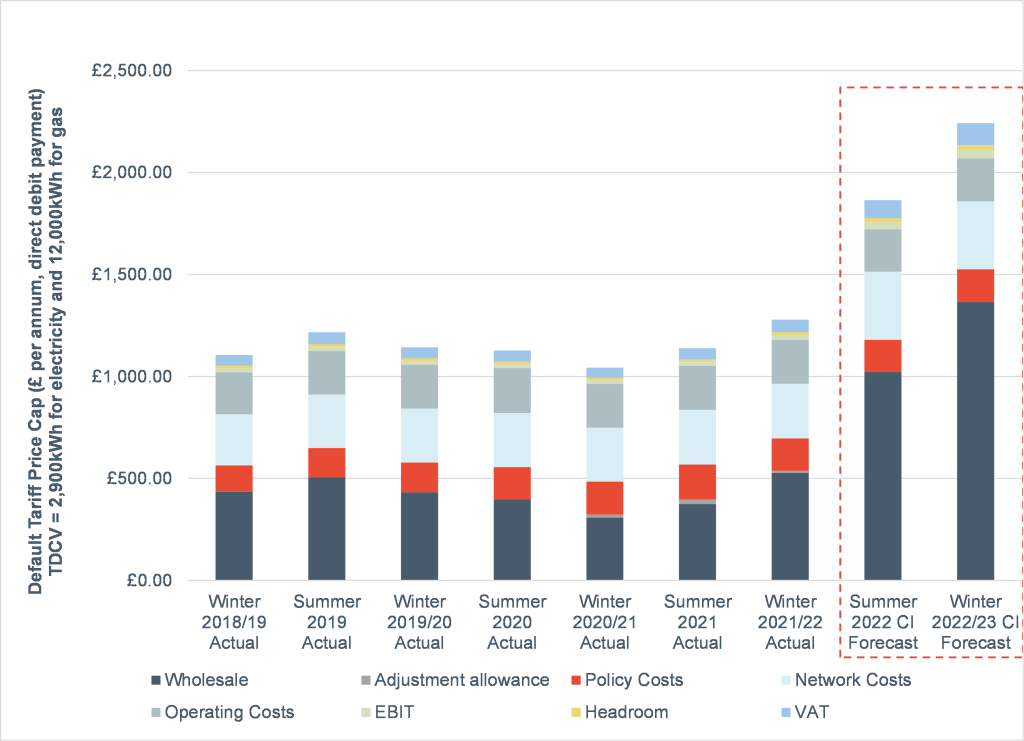

Following further highs in wholesale prices and the costs associated with the raft of supplier failures seen in the last few months, Cornwall Insight is forecasting that the domestic default tariff price cap for Summer 2022 will increase to approximately £1,865 per annum for a typical dual fuel customer, with the potential for further increases between now and February 2022 – when the cap is announced by Ofgem – still apparent. This represents an increase of just under 50% on the current Winter 2021-22 cap level of £1,277 per annum – itself a record high – and an increase of around 12% on our previous estimate of the Summer 2022 cap from October 2021.

With wholesale prices having surged beyond the records seen at the start of October due to ongoing supply concerns for electricity and gas, geopolitical pressures affecting the European gas market and colder weather associated with the winter season, our forecasts reflect these prevailing conditions. Furthermore, our current forecast for the Winter 2022-23 default tariff price cap stands at approximately £2,240 per annum, although we note that this figure may face considerable change before it is formally announced in August 2022.

Default tariff price cap for a typical dual fuel domestic customer, actual & Cornwall Insight forecasts

Cornwall Insight’s assessment of the total cost associated with those suppliers that have gone through the Supplier of Last Resort (SOLR) regime – which does not include Bulb – is approximately £2.4bn. Based upon our assumption that those customers’ new suppliers will have had to purchase gas and electricity on the wholesale market to meet this new demand, the costs associated with these trades – compared to the wholesale cost element of Ofgem’s default tariff price cap – represent the lion’s share of this sum.

Those acquiring suppliers will then be able to apply through Ofgem to recover the costs of taking responsibility for these customers through claims under the Last Resort Supply Payment (LRSP) mechanism. This is a well-established approach through which the cost of these claims are recovered through the network charges paid by domestic gas and electricity customers.

This £2.4bn therefore equates to approximately £90 per household, assuming 27mn customers from which this sum can be recovered. However, our forecasts for Summer 2022 and Winter 2022-23 already include c. £30 per annum worth of costs associated with the former suppliers. This is based upon indicative 2022-23 charging statements from the gas distribution operators and our own assessment of the impact of mutualisation associated with the Renewables Obligation low carbon generation support scheme. With charging statements to follow from the other energy network companies, we therefore anticipate the remaining costs associated with the wave of supplier exits – currently forecast to be an additional c. £60 per annum – to be crystallised within the coming months.

Dr Craig Lowrey, Senior Consultant, Cornwall Insight

“With Ofgem examining a wide range of potential reforms to both the cap and the way in which the costs associated with supplier failures are recovered, we note that there is still a large amount of uncertainty relating to the level and structure of the cap. However, with the energy supply sector still dealing with the exit of more than two dozen companies in a matter of weeks, the need to ensure resilience across the entire market is evident. Furthermore, it is not solely domestic customers that are dealing with these new highs in energy costs, as businesses will face their own set of challenges without the protection afforded by the default tariff price cap.”

Notes to Editors

For more information, please contact: Vicky Merrison at v.merrison@cornwall-insight.com

To link to our website, please use: https://www.cornwall-insight.com/

About the Cornwall Insight Group

Cornwall Insight is the pre-eminent provider of research, analysis, consulting and training to businesses and stakeholders engaged in the Australian, Great British, and Irish energy markets. To support our customers, we leverage a powerful combination of analytical capability, a detailed appreciation of regulation codes and policy frameworks, and a practical understanding of how markets function.

You may also be interested in…

Insight Services | Domestic market share survey – Energy suppliers market share overview

The ‘Domestic market share survey’ gives you an up to date overview of the retail energy market. It identifies the active suppliers, new entrants, overall market growth, national and regional changes in electricity, gas and dual fuel accounts. Click through to find out more.