The energy crisis has pushed up prices for drivers charging their EVs on the public network. A depressing milestone was passed last month, when a public charging operator (CPO) had to increase its prices to a new high of £1/kWh. Many others have also put through significant increases, as regular readers of our EV Insight Service will know. Average ultra-rapid charging prices were up 8p last month to 67p/kWh. Both rapid and ultra-rapid charging are on average now significantly more expensive than refilling a petrol or diesel car.

Since the £1/kWh rate hit the headlines, the picture has cleared on how the government’s Energy Bill Relief Scheme (EBRS) will support non-domestic bills. We saw the first CPO put through rate reductions this week as a result, and others will surely follow suit (to varying degrees) as they work with their energy providers to understand how the support will affect their supply contracts. To understand how this support could flow through into prices, it’s worth looking briefly at how CPOs reflect the costs they face in the rates they pass onto drivers.

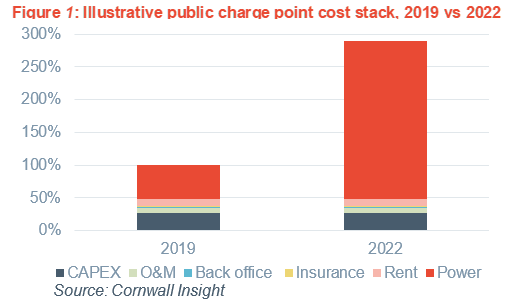

While prices have increased, they have not risen at the same rate as wholesale electricity costs, and in practice CPO prices will not be a simple track of the wholesale market. Energy inputs will depend on the type and length of supply contracts, and CPOs have other costs to recover from drivers, including asset costs, rent and operational costs (Figure 1). CPOs will then make commercial decisions on how to recover these costs from drivers – revenue for CPOs comes from utilisation of their networks, and pricing decisions need to support increased utilisation, both at a particular network and in a broader sense through supporting the transition to EVs. Break-even and profitability targets will also depend on individual business plans. As we know from CPO communications around recent price changes, many have been taking the decision to absorb as far as possible higher commodity costs, rather than pass them onto drivers. As our illustrative breakdown of CPO costs in Figure 1 shows, however, the energy element of the cost stack now substantially dwarfs other components.

So, what impact will the EBRS have on this price environment? Unlike the domestic Energy Price Guarantee, the EBRS does not guarantee businesses a fixed unit rate for delivered energy, and instead provides a discount to the wholesale element of the bill up to a maximum reduction £34/MWh. There will be differences in how this support feeds through to end users based on contract types. The EBRS will help with costs, but will not fully undo the substantial increase in prices seen by CPOs this year. Source London reduced its public charging prices last week as a result of the EBRS, telling its customers that the government support would “reduce some of our commodity costs”. Depending on the EV customer’s membership status, the reduction in price ranges from a 16% to a 6% cut. If they are in a financial position to be able to do so, other CPOs will likely follow in putting through some level of cost reduction. Following its price rise to £1/kWh, Osprey said it hoped to be able to pass on a saving to customers once its energy supplier had updated prices following the EBRS, which it expected to happen some time in October. Others that have been struggling to absorb rising commodity costs may use the support to maintain operations and delay further price rises. However the market responds, this may only be a six-month reprieve: decisions are yet to be made on what sectors will continue to receive support, and what this support will look like in the future.

On 16 November we will be hosting an in-person EV event in London addressing the key challenges facing the EV transition today. We’re excited to be joined by guest speakers from: Autotrader; Octopus EV; Energy Hub; Total Energies; Energy Systems Catapult; Paythru; plus more TBC. If you would like to attend this free event, please fill out this brief form and we will provide further details.