The Australian Renewable Energy Agency (ARENA) was one of those rare institutions that managed to survive the political energy battles over the last decade. Initially established in 2012, ARENA has dispensed over $1.9b in funding to date to support renewable technologies, often at the ‘pre-commercial’ stage. The ARENA funding gives new technologies a chance to prove their viability for eventual commercial use by the wider market.

Tracking where ARENA has provided funding provides an insight into what nascent technologies have been deemed important enough to warrant ARENA funding. This Chart of the week looks at a few trends from the ARENA funding over time, pinpointing future technologies that may shape the Australian energy market transition.

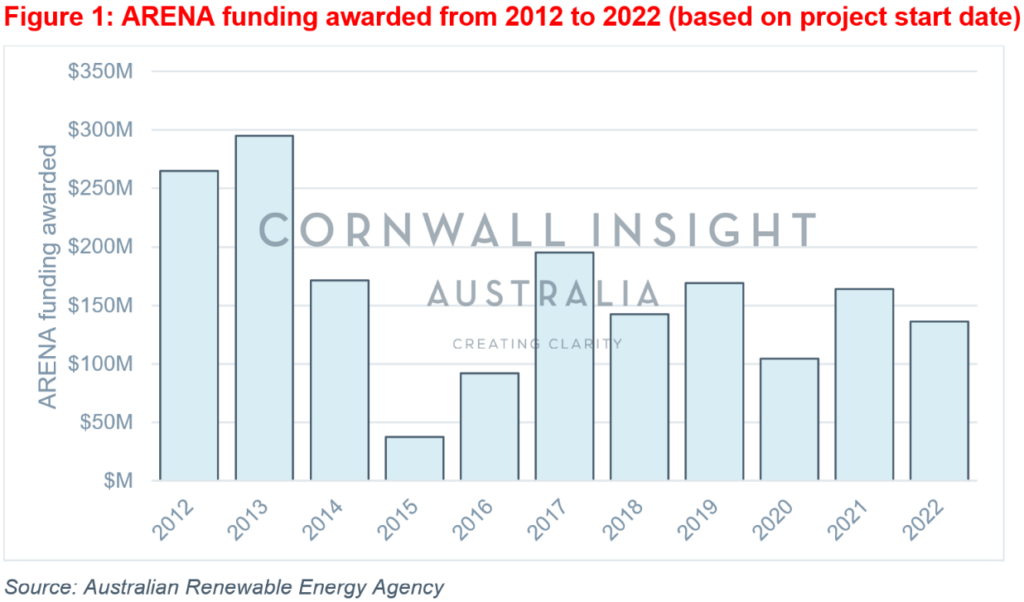

Figure 1 shows the funding awarded by ARENA since 2012 based on the project start date. As seen in this figure, the funding varied wildly from year to year at the scheme’s start, with large outlays in the first few years followed by relative droughts over the middle of the last decade. Since 2017, funding awards have been largely steady.

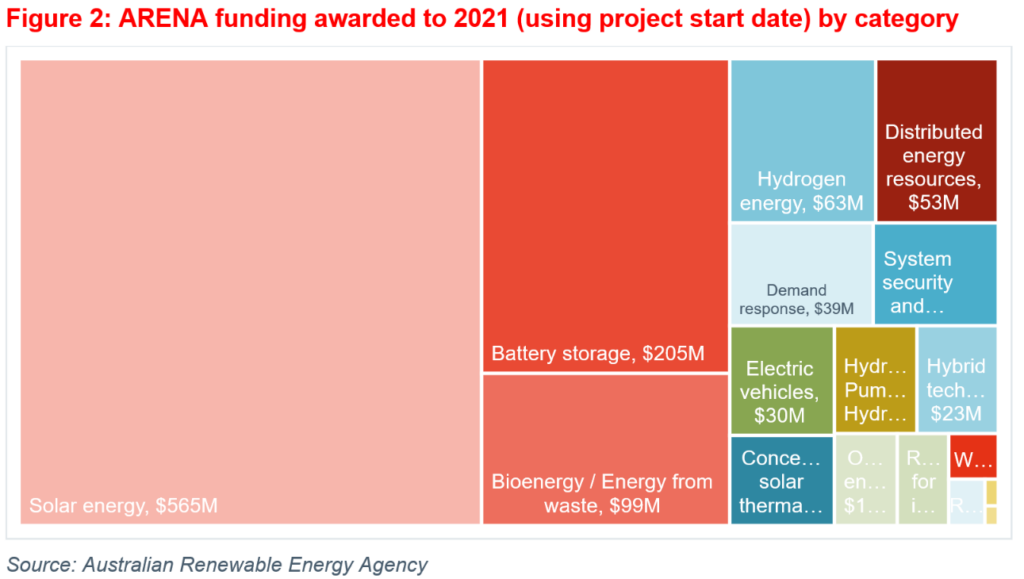

Not surprisingly, the mix of projects receiving funding has changed over time. For the period until 2021, funding was dominated by solar energy projects with also significant contribution to battery storage projects (see Figure 2).

Note that the funding figures above for solar include three projects that were awarded significant funding: $166.7M for an AGL solar project in Broken Hill, $102M for the Moree Solar Farm, and $129M for the Australian Centre for Advanced Photovoltaics (ACAP) for research and training.

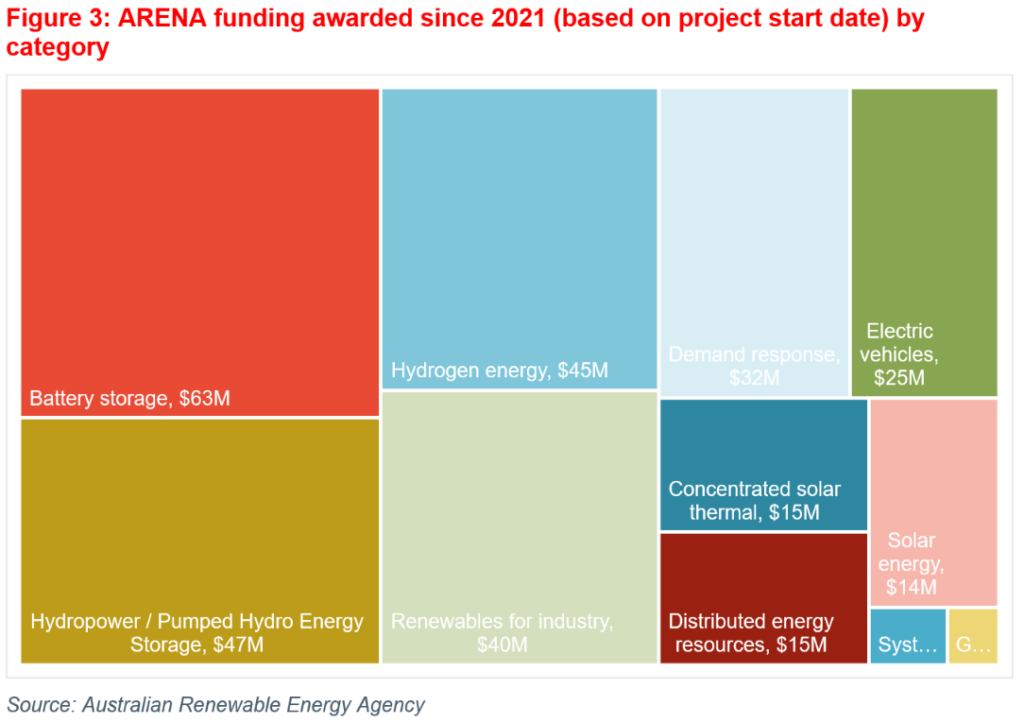

Looking at Figure 3, representing a more recent history, we can see that since 2021 (inclusive), the funding mix has changed significantly. More recently, higher proportions of funding have been awarded to battery storage, hydro/pumped-hydro, hydrogen, electric vehicles, demand response and solar thermal.

Again, this is not a surprise, as these technologies and initiatives will be part of the energy transition. An interesting observation is that solar energy has dropped down the scale significantly, perhaps proven as a commercial technology, thus not warranting ARENA funding to the same extent.

Overall, this points to the technologies that may shape the future of Australian energy systems under current government settings. It will be interesting to see whether funding for ARENA is affected by the upcoming Federal budget next week.

Cornwall Insight Australia release a monthly Executive Energy Summary highlighting key market developments in the industry in a concise brief – a ‘cheat sheet’ to keep on top of the market. Please contact us via enquiries@cornwall-insight.com.au to receive a free sample.