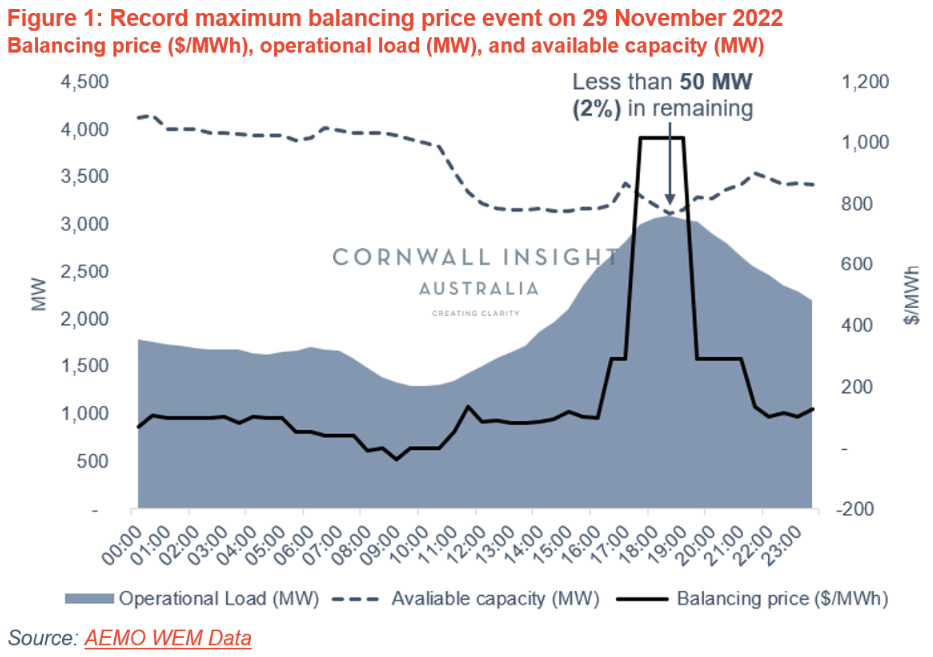

For the first time in the history of the Western Australian Wholesale Electricity Market (WEM), the balancing price reached the maximum price limit of $1,018/MWh between 5:30pm and 7:30pm on Tuesday, 29 November 2022.

This came one month after the state-owned Muja C Unit 5 coal power station was closed. The Collie coal power station was also on outage due to significant coal shortages in WA. These two facilities combined delivered approximately 10% of total market generation in 2020-211.

A large quantity of outages combined with high temperatures drive this event. During this event, all available facilities were generating, including diesel facilities that are rarely dispatched. At one point, there was less than 50 MW, or 2% in remaining reserve2.

There is an immediate need for new dispatchable capacity as coal is retired

This summer, the Australian Energy Market Operator (AEMO) issued a tender for additional reserve capacity to mitigate the risk of a potential capacity shortfall due to a combination of coal closures, coal supply constraints, and extended generator outages.

More state-owned coal closures are soon to follow, with Muja C Unit 6 scheduled to close in October 2024. All remaining state-owned coal power stations are to be retired by 2030.

At the same time, the 2022 AEMO WA Gas Statement of Opportunities models a scenario where Bluewaters – the last remaining privately owned coal power station in the state, closes as early as 2023 due to the impact of coal supply shortages.

Storage provides dispatchable capacity and contributes to emissions reduction

Gas-fired generation can provide dispatchable capacity as coal is retired. Nonetheless, this has implications for emissions-reduction targets. WA has some of the best wind and solar resources in the world. The state has world-leading uptake of rooftop PV and a growing pipeline of large-scale renewables projects. A significant amount of storage is required to store this energy for use during peak demand periods.

Cornwall Insight has Storage Investment Models that provide in-depth revenue forecasting and optimisation services. In addition, we have NEM and WEM market models based on market-validated assumptions and sound power systems principles. For more information on the energy market and power systems modelling or other bespoke consultancy products, please contact enquiries@cornwall-insight.com.au.

12022 Wholesale Electricity Market Electricity Statement of Opportunities, June 2022

2This considers the capacity required for spinning reserve and load following.