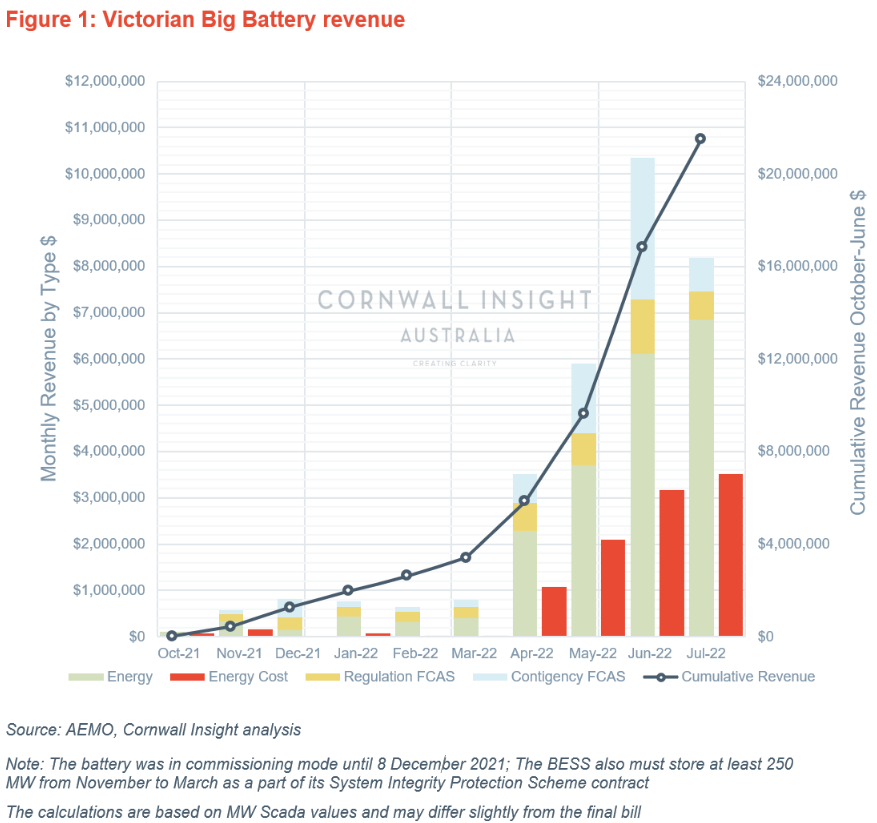

The Victorian Big Battery (VBB) in Geelong, Victoria, is currently the largest commissioned battery in the NEM at 300 MW/450 MWh. In Q2 2022, VBB, and its owner Neoen, posted an estimated AEMO wholesale net revenue of just over $13 million for the three-month period.

It is important to note that VBB may not fully realise this value due to other revenue sources/contracts that it may hold; however, it represents just over 8% of the project’s finance costs (costing $160m for the design, construction, and operation). Great news for the project, which recovered from a fire on its first day of commissioning nearly a year ago, which destroyed two of its Tesla Megapacks on its first testing day (31 July 2021).

The VBB is part of the System Integrity Protection Scheme (SIPS) initiated by the Victorian government to bring forward critical transmission investments. As part of the scheme, the battery has a 250 MW contract with AEMO, which sees it reserve ~80% of its capacity to allow the energy market operator to increase the power flow through the Victoria-New South Wales Interconnector (VNI) over the next decade of Australian summers (November-March).

Therefore, the start of Q2 marks the first period VBB can operate at its full potential.

As we have discussed in previous Charts of the week, Q2 2022 saw both commodity and electricity prices soaring in Australia, particularly in the evening peaks, where the pricing situation has fundamentally changed with higher cost generators altering their price band and MW values to accommodate for modern times. Opportunities for energy arbitrage have never been more apparent.

Victorian average prices in Q2 2022 were $224/MWh. However, within the day, the spread was large. Super-peak prices (6 pm-8 pm) averaged around $322/MWh, while midday prices (10 am-2 pm) averaged around $166/MWh. A potential arbitrage value of nearly double at $156/MWh.

The VBB had a clear trend of charging during overnight lows at 2:30 am until 5 am, charging at least 50 MW during 36% of these intervals in Q2. Dispatching a portion of it during the morning peak; charging again from 10 am until 1 pm and maximising its potential in the afternoon at 5 pm-7 pm, discharging at least 50 MW in 42% of this time interval in Q2. This number hovers around 9-11% for all intervals mentioned above when taking into account charges and discharges at 150 MW or greater.

When taking a sample number of 50 MW, the battery charged at least 50MW at a price of $133/MWh and discharged at $332/MWh, an arbitrage value of $199 per MW.

As shown in the chart below, energy arbitrage represented ~61% of VBB revenue in Q2 2022, accumulating $12.1m of revenue in energy, while FCAS contributed $7.6m. The arbitrage continued to a greater extent in July, with the BESS an 84% energy to FCAS revenue ratio. Since its release from SIPS, it is estimated the project has a revenue of $27.9m and an expense bill of $9.7m.

It is also worth noting that the Administered Price Cap and ultimately the market suspension in June 2022 likely reduced its overall revenue to an extent. During the suspension, it was operated near constantly during the week (noting that the battery has not filed for compensation claims at this point as per AEMC public documentation).

The high turnover in Q2 2022 is not limited to VBB. Estimates for Hornsdale PR were around $10 million, and Wandoan at just under $5mil in Q2 2022. On a captured prices front, state-wide battery generation weighted average prices sat at $992/MWh in QLD, $653/MWh in NSW, $585/MWh in SA, and $363/MWh in VIC. A significant increase in recent history. Given that Q2 2021 saw FCAS account for 78% of revenue, it appears there has been a significant change in opportunities and focus.

In broader terms, batteries are a special asset in the NEM. It has a limited capacity to charge or discharge energy at any point in time. As a result, bidding decisions have a big impact on future revenue. There is still much to learn about how to operate batteries most profitably.

The outlook for prices continues to show high prices over the next 12 months. Gas forward prices are still showing above $40/GJ in most economies into 2023, which means that marginal run costs will likely keep peak time prices at elevated levels. This represents a continued opportunity for energy arbitrage between bimodal daytime prices and peak time.

For more information on how the market dynamics could impact storage in the NEM, Cornwall Insight can provide technical advisory and modelling services for energy storage projects and future market scenarios. If you would like further information, please contact us at enquiries@cornwall-insight.com.au.