The announcement on Friday that QEnergy and Mojo Power will no longer provide retail services illustrates the battering Australian electricity retailers have faced over the last year. High hedging costs, especially for non-vertically integrated retailers, have seen smaller retailers hit the wall, such as Elysian Energy, Enova Energy, and Power Club. Yet larger retailers are not the sole beneficiaries of this retail market shake-up.

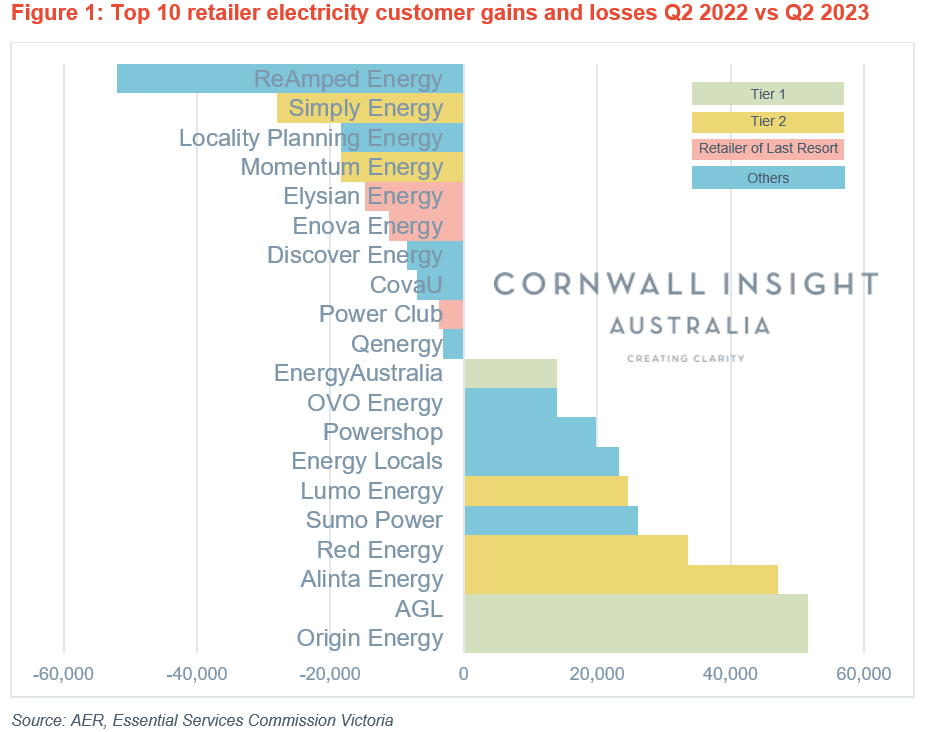

In our Chart of the week, we take a snapshot of electricity retailer customer churn across the NEM, listing the top 10 retailers for gains and losses between Q2 2023 and the corresponding quarter last year.

From this snapshot, some generation observations can be made:

- Tier 1 legacy retailers (AGL, Origin Energy, Energy Australia) have benefitted from the recent market churn. This is not a surprise as these retailers can back their retailer customer books with their extensive generation portfolios.

- For Tier 2 retailers, which are non-legacy retailers with their own generation, churn is more mixed, with Red Energy (Snowy Hydro) and Lumo Energy (Snowy Hydro) and Alinta Energy increasing their customer numbers while Simply Energy (Engie) and Momentum (Hydro Tasmania) have decreased.

- Snowy Hydro (through Red Energy and Lumo Energy together) would have combined to have increased the number of customers by more than Origin or AGL.

- The retailers that have suspended trading (with their customers transferred according to Retailer of Last Resort processes) are fairly small relative to the market.

- The biggest drop in customers was for ReAmped Energy, which encouraged their customers to leave at the height of the energy pricing crisis a year ago, triggering a potential investigation by the regulator. Despite this, ReAmped Energy still maintains an active electricity retail licence.

It is important to note that a retailer losing customers does not necessarily mean trouble is on the cards. Retailers may want to align their generation and retail portfolios, which may create a more stable retailer that is less reliant on external hedges. Furthermore, as retail margins are squeezed, retailers may be moving customers from highly discounted to more sustainable pricing plans. This should create more opportunities for churn if retailers can present compelling offers.

Significant market events like these are captured in Cornwall Insight Australia’s Executive Energy Summary. The summary is a low-cost monthly report that provides subscribers with an analysis of that month’s most impactful market events. Please contact us at enquiries@cornwall-insight.com.au for a free sample and introductory pricing we have available.